[ad_1]

bjdlzx

This is a Z4 Energy Research Pre-Call Note

Z4 Energy Research

Magnolia Oil & Gas Corporation (NYSE:MGY) Guidance: Up, again.

- 2022 Production: They’re guiding to a busy year-end as they note setting them up for a strong start to 2023.

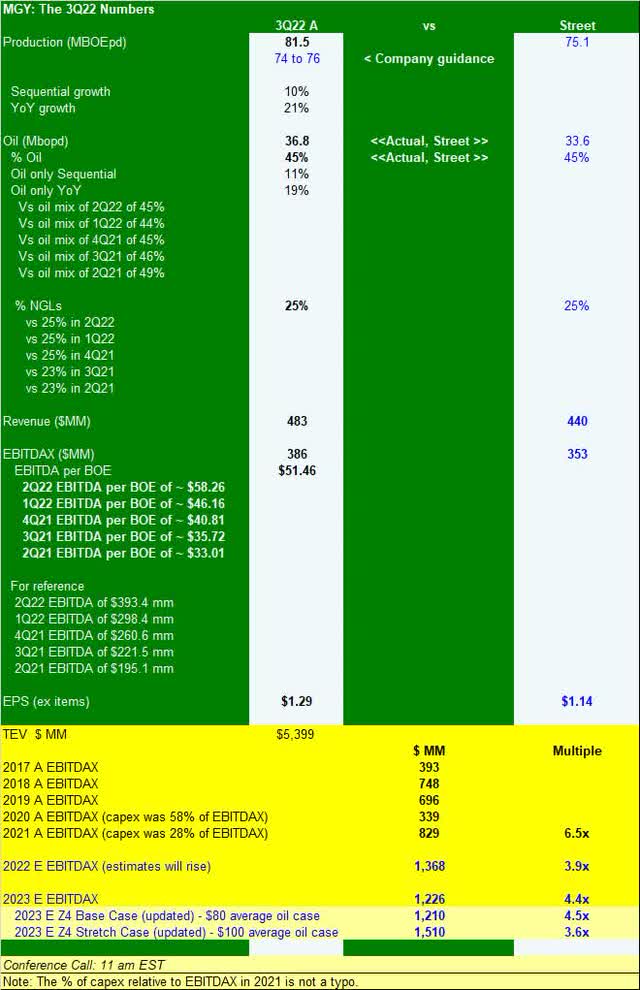

- They guided 4Q22 to a range of 77 to 79 MBOEpd, a little sequential slippage due to completion timing but still ahead of current consensus expectation of 76.7 MBOEpd. Taken with the first 9 months’ actuals this implies full year on mid production for 2022 of 76.4 MBOEpd, up almost 16% from 2021 and ahead of prior management color of 12 to 14% (guidance which had already been boosted this year due to strong well performance. This is also above current 2022 Street expectations of 74.4 MBOEpd.

- Please note that for modeling purposes we were at 80 MBOEpd for next year, which would imply less than 5% growth, and as such, given multiple quarters of better than expected well performance, our numbers are under review for a potential increase. We also note that the Street, which at the time of the last call was just below us for 2023 at 79 MBOEpd, is now up to and as of yesterday were up to 80.1 MBOEpd.

- Capex: Previously guided as close to $400 mm, and we don’t see a significant uptick with the numbers in the release. Non-op drilling could boost They continue to run two rigs with one dedicated to Giddings “development area” drilling and one flipping back and forth between Giddings, including some step out wells, and the oilier Karnes position.

Other Notable Numbers and Items from the Quarter:

- MGY realized 102% of WTI in the quarter. Most of upstream names in the U.S. see a $3 to $5 discount to WTI.

- Capex was just 30% of EBITDAX for the quarter. They are achieving growth without jumping up spending.

- Free cash flow of $234 mm vs $201 mm consensus.

- LOE for the quarter was $4.63 per BOE vs $4.83 in 2Q22 despite industry-wide inflationary pressures. Other operating costs were well in check as well and in fact, EBITDAX was just 2% short of a quarterly record (2Q22 having set the record) despite a $15 sequential decline in oil prices.

- They remain, by policy, unhedged.

- Brian Corales, who we check in with every few months to make sure all is on track, has been promoted to CFO. Brian is a former sell-side guy, extremely well-versed in the story, really gets what the buyside needs to see, and we applaud the move. Hopefully he will still take my calls.

Mixed Emotions Quote Watch: “The most recent quarter was filled with mixed emotions. We are humbled by our continued strong financial and operating results and performance, yet deeply saddened by the recent passing of Steve Chazen, Magnolia’s founder and former CEO. I am incredibly grateful for Steve’s guidance and counsel, his steadfast leadership and importantly his friendship. We expect his legacy to continue to live on through Magnolia for years to come,” said President and CEO Chris Stavros. “The principles of the business model that Steve established during Magnolia’s founding over four years ago are expected to remain unchanged. We will continue our discipline around capital spending, while maintaining low levels of debt. We expect our record of achieving moderate annual production growth, while generating significant free cash flow and strong pre-tax margins to continue.”

Operational Highlights: Better wells, cheaper wells.

- The much stronger than expected quarterly production was attributed to better than expected well results in both Karnes and Giddings along with slightly higher non-operated activity. We’ve been anticipating a pickup at Karnes (likely this is EOG) for some time now, and this makes sense that more stable prices are seeing an uptick in this higher-return, well-delineated play.

- Management notes that D&C costs per foot are down 26% this year despite inflation, as they put more wells on each pad and hone their process.

Balance Sheet: Fortress

- At quarter-end, cash had grown to $690 mm and $390 mm of senior debt. They continue to have nothing drawn on the balance sheet, and as they’ve often noted in the past, they have no intention of adding more debt.

Return of Capital:

- Share repurchase program remains one of the most active in the space:

- MGY has a goal of repurchasing 1% or more of shares outstanding each quarter.

- In 3Q22 they took in 3 mm additional shares and their count is down 8% on a YoY basis (or roughly double the stated minimum).

- As the stock price moves back to new highs and as their private equity component is further reduced, we would expect them to gradually reduce the share repurchases in favor of a larger but still sustainable base dividend. We do not expect them to move to a formulaic variable dividend at this time.

- Dividends:

- We expect the base dividend here to slowly increase over time, and with today’s release they announced an expectation of growing the base dividend by at least 10% per year. The implied yield on the current dime per quarter rate is 1.6%.

- We expect the company to not simply grow cash on the balance sheet, and, if they do not find attractive acquisitions, to likely send some of their cash hoard back to shareholders, likely with the 4Q22 report early next year, in the form of a special dividend.

Nutshell: This was a monster quarter by most definitions. We will miss Chazen’s unvarnished industry commentary on the quarter calls going forward and just be grateful to have been around to watch him run with a plan to significantly under-spend cash flow far before it was in vogue. What a company he has forged.

Looking ahead, Magnolia Oil & Gas Corporation’s guidance is again above us and above Street. Estimates should rise in the wake of the quarter for 2022 and 2023. The balance sheet is even more of a fortress now, and 4Q will see more cash pile up. We do think there’s a decent possibility that some of that cash will be returned to shareholders in the form of a special dividend.

As noted near the bottom of the table above, MGY trades at 4.5x our 2023 Base Case ($80 oil and $5 gas) EBITDAX. We view this as low considering: their cash horde, strong growth at a time when others achieve excess free cash flow only via maintenance mode, modest yet easily growable base dividend, and constant and significant share buyback. We also expect to be revising our 2023 numbers post-call, meaning it’s really trading below that level. MGY remains our second-largest position, where we have an average cost of $10.96.

[ad_2]

Source link