[ad_1]

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Vinte Viviendas Integrales, S.A.B. de C.V. (BMV:VINTE) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Vinte Viviendas Integrales. de

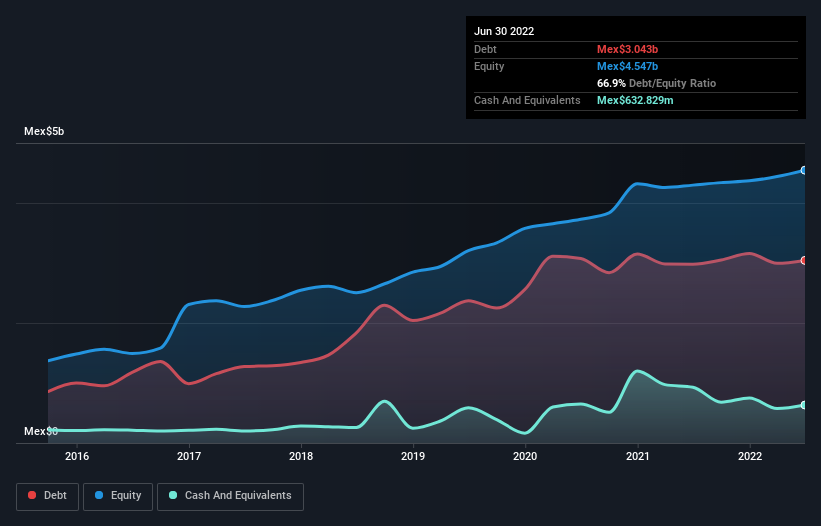

What Is Vinte Viviendas Integrales. de’s Net Debt?

The chart below, which you can click on for greater detail, shows that Vinte Viviendas Integrales. de had Mex$3.04b in debt in June 2022; about the same as the year before. However, it does have Mex$632.8m in cash offsetting this, leading to net debt of about Mex$2.41b.

A Look At Vinte Viviendas Integrales. de’s Liabilities

The latest balance sheet data shows that Vinte Viviendas Integrales. de had liabilities of Mex$1.19b due within a year, and liabilities of Mex$3.67b falling due after that. Offsetting this, it had Mex$632.8m in cash and Mex$449.8m in receivables that were due within 12 months. So its liabilities total Mex$3.77b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Vinte Viviendas Integrales. de has a market capitalization of Mex$6.93b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Vinte Viviendas Integrales. de’s net debt is 4.4 times its EBITDA, which is a significant but still reasonable amount of leverage. But its EBIT was about 15.3 times its interest expense, implying the company isn’t really paying a high cost to maintain that level of debt. Even were the low cost to prove unsustainable, that is a good sign. If Vinte Viviendas Integrales. de can keep growing EBIT at last year’s rate of 19% over the last year, then it will find its debt load easier to manage. When analysing debt levels, the balance sheet is the obvious place to start. But it is Vinte Viviendas Integrales. de’s earnings that will influence how the balance sheet holds up in the future. So if you’re keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Considering the last three years, Vinte Viviendas Integrales. de actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

Neither Vinte Viviendas Integrales. de’s ability to convert EBIT to free cash flow nor its net debt to EBITDA gave us confidence in its ability to take on more debt. But its interest cover tells a very different story, and suggests some resilience. We think that Vinte Viviendas Integrales. de’s debt does make it a bit risky, after considering the aforementioned data points together. That’s not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it. To that end, you should learn about the 3 warning signs we’ve spotted with Vinte Viviendas Integrales. de (including 2 which are potentially serious) .

If you’re interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re helping make it simple.

Find out whether Vinte Viviendas Integrales. de is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free Analysis

[ad_2]

Source link