[ad_1]

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, VOXX International Corporation (NASDAQ:VOXX) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for VOXX International

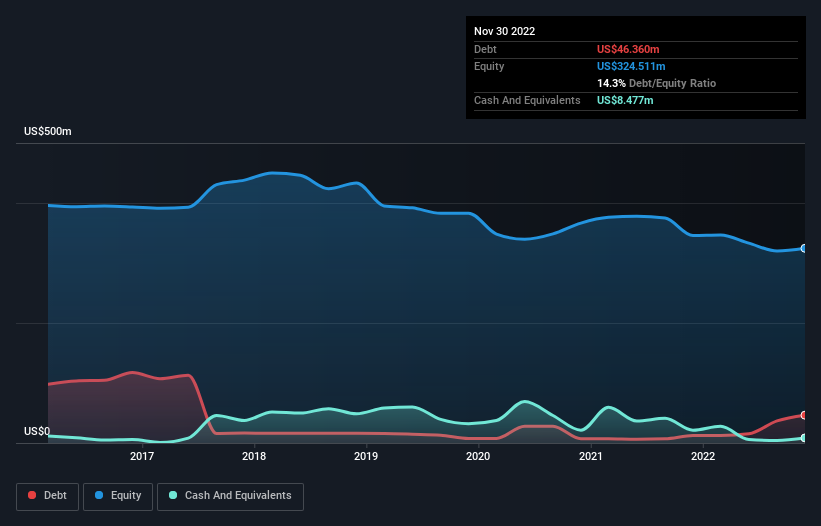

What Is VOXX International’s Net Debt?

As you can see below, at the end of November 2022, VOXX International had US$46.4m of debt, up from US$12.3m a year ago. Click the image for more detail. On the flip side, it has US$8.48m in cash leading to net debt of about US$37.9m.

A Look At VOXX International’s Liabilities

Zooming in on the latest balance sheet data, we can see that VOXX International had liabilities of US$167.5m due within 12 months and liabilities of US$74.4m due beyond that. Offsetting these obligations, it had cash of US$8.48m as well as receivables valued at US$100.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$133.5m.

This deficit isn’t so bad because VOXX International is worth US$240.2m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine VOXX International’s ability to maintain a healthy balance sheet going forward. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

In the last year VOXX International had a loss before interest and tax, and actually shrunk its revenue by 12%, to US$561m. We would much prefer see growth.

Caveat Emptor

Not only did VOXX International’s revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). To be specific the EBIT loss came in at US$8.8m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled US$45m in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we’ve identified 1 warning sign for VOXX International that you should be aware of.

Of course, if you’re the type of investor who prefers buying stocks without the burden of debt, then don’t hesitate to discover our exclusive list of net cash growth stocks, today.

What are the risks and opportunities for VOXX International?

VOXX International Corporation, together with its subsidiaries, designs, manufactures, and distributes automotive electronics, consumer electronics, and biometric products in the United States, Europe, and internationally.

View Full Analysis

Rewards

-

Trading at 42.7% below our estimate of its fair value

-

Earnings are forecast to grow 72.89% per year

-

Earnings have grown 4.1% per year over the past 5 years

Risks

-

Has less than 1 year of cash runway

View all Risks and Rewards

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

[ad_2]

Source link