[ad_1]

It’s only natural that many investors, especially those who are new to the game, prefer to buy shares in ‘sexy’ stocks with a good story, even if those businesses lose money. But as Warren Buffett has mused, ‘If you’ve been playing poker for half an hour and you still don’t know who the patsy is, you’re the patsy.’ When they buy such story stocks, investors are all too often the patsy.

So if you’re like me, you might be more interested in profitable, growing companies, like Netanel Group (TLV:NTGR). While that doesn’t make the shares worth buying at any price, you can’t deny that successful capitalism requires profit, eventually. In comparison, loss making companies act like a sponge for capital – but unlike such a sponge they do not always produce something when squeezed.

See our latest analysis for Netanel Group

Netanel Group’s Improving Profits

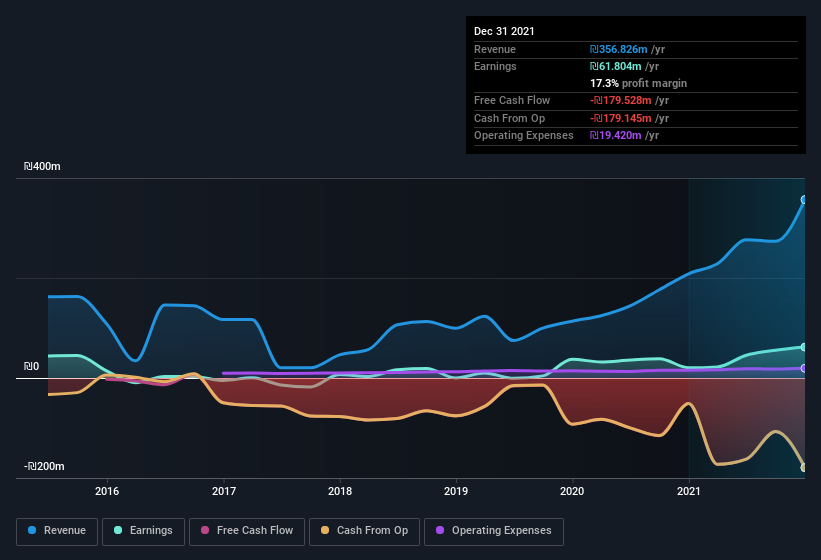

In business, though not in life, profits are a key measure of success; and share prices tend to reflect earnings per share (EPS). So like the hint of a smile on a face that I love, growing EPS generally makes me look twice. It is therefore awe-striking that Netanel Group’s EPS went from ₪0.73 to ₪2.19 in just one year. When you see earnings grow that quickly, it often means good things ahead for the company. But the key is discerning whether something profound has changed, or if this is a just a one-off boost.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. The good news is that Netanel Group is growing revenues, and EBIT margins improved by 2.7 percentage points to 19%, over the last year. That’s great to see, on both counts.

You can take a look at the company’s revenue and earnings growth trend, in the chart below. Click on the chart to see the exact numbers.

Since Netanel Group is no giant, with a market capitalization of ₪334m, so you should definitely check its cash and debt before getting too excited about its prospects.

Are Netanel Group Insiders Aligned With All Shareholders?

I always like to check up on CEO compensation, because I think that reasonable pay levels, around or below the median, can be a sign that shareholder interests are well considered. For companies with market capitalizations under ₪679m, like Netanel Group, the median CEO pay is around ₪1.4m.

Netanel Group offered total compensation worth ₪1.1m to its CEO in the year to . That seems pretty reasonable, especially given its below the median for similar sized companies. While the level of CEO compensation isn’t a huge factor in my view of the company, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. I’d also argue reasonable pay levels attest to good decision making more generally.

Is Netanel Group Worth Keeping An Eye On?

Netanel Group’s earnings have taken off like any random crypto-currency did, back in 2017. With rocketing profits, its seems likely the business has a rosy future; and it may have hit an inflection point. Meanwhile, the very reasonable CEO pay reassures me a little, since it points to an absence profligacy. While I couldn’t be sure without a deeper dive, it does seem that Netanel Group has the hallmarks of a quality business; and that would make it well worth watching. You should always think about risks though. Case in point, we’ve spotted 4 warning signs for Netanel Group you should be aware of, and 2 of them shouldn’t be ignored.

Of course, you can do well (sometimes) buying stocks that are not growing earnings and do not have insiders buying shares. But as a growth investor I always like to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

[ad_2]

Source link