[ad_1]

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it completely lacks a track record of revenue and profit. But as Warren Buffett has mused, ‘If you’ve been playing poker for half an hour and you still don’t know who the patsy is, you’re the patsy.’ When they buy such story stocks, investors are all too often the patsy.

In contrast to all that, I prefer to spend time on companies like Khind Holdings Berhad (KLSE:KHIND), which has not only revenues, but also profits. While that doesn’t make the shares worth buying at any price, you can’t deny that successful capitalism requires profit, eventually. Loss-making companies are always racing against time to reach financial sustainability, but time is often a friend of the profitable company, especially if it is growing.

Check out our latest analysis for Khind Holdings Berhad

How Fast Is Khind Holdings Berhad Growing Its Earnings Per Share?

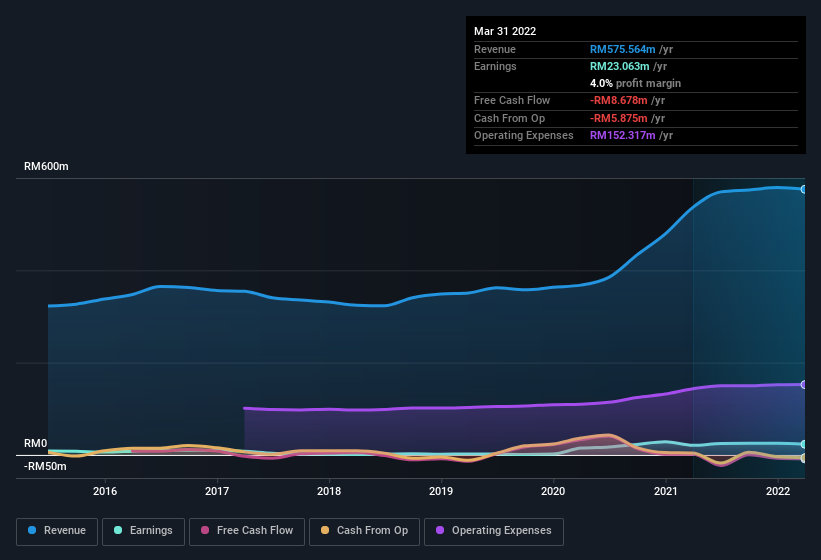

In the last three years Khind Holdings Berhad’s earnings per share took off like a rocket; fast, and from a low base. So the actual rate of growth doesn’t tell us much. Thus, it makes sense to focus on more recent growth rates, instead. Khind Holdings Berhad boosted its trailing twelve month EPS from RM0.52 to RM0.58, in the last year. That’s a 11% gain; respectable growth in the broader scheme of things.

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). While we note Khind Holdings Berhad’s EBIT margins were flat over the last year, revenue grew by a solid 7.3% to RM576m. That’s a real positive.

The chart below shows how the company’s bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

Since Khind Holdings Berhad is no giant, with a market capitalization of RM118m, so you should definitely check its cash and debt before getting too excited about its prospects.

Are Khind Holdings Berhad Insiders Aligned With All Shareholders?

Many consider high insider ownership to be a strong sign of alignment between the leaders of a company and the ordinary shareholders. So we’re pleased to report that Khind Holdings Berhad insiders own a meaningful share of the business. Actually, with 37% of the company to their names, insiders are profoundly invested in the business. I’m always comforted by solid insider ownership like this, as it implies that those running the business are genuinely motivated to create shareholder value. Of course, Khind Holdings Berhad is a very small company, with a market cap of only RM118m. So despite a large proportional holding, insiders only have RM44m worth of stock. That might not be a huge sum but it should be enough to keep insiders motivated!

Is Khind Holdings Berhad Worth Keeping An Eye On?

One important encouraging feature of Khind Holdings Berhad is that it is growing profits. If that’s not enough on its own, there is also the rather notable levels of insider ownership. That combination appeals to me, for one. So yes, I do think the stock is worth keeping an eye on. We should say that we’ve discovered 1 warning sign for Khind Holdings Berhad that you should be aware of before investing here.

Of course, you can do well (sometimes) buying stocks that are not growing earnings and do not have insiders buying shares. But as a growth investor I always like to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

[ad_2]

Source link