[ad_1]

While Mattel, Inc. (NASDAQ:MAT) shareholders are probably generally happy, the stock hasn’t had particularly good run recently, with the share price falling 22% in the last quarter. But that doesn’t change the fact that the returns over the last three years have been pleasing. After all, the share price is up a market-beating 49% in that time.

Now it’s worth having a look at the company’s fundamentals too, because that will help us determine if the long term shareholder return has matched the performance of the underlying business.

See our latest analysis for Mattel

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it’s a weighing machine. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

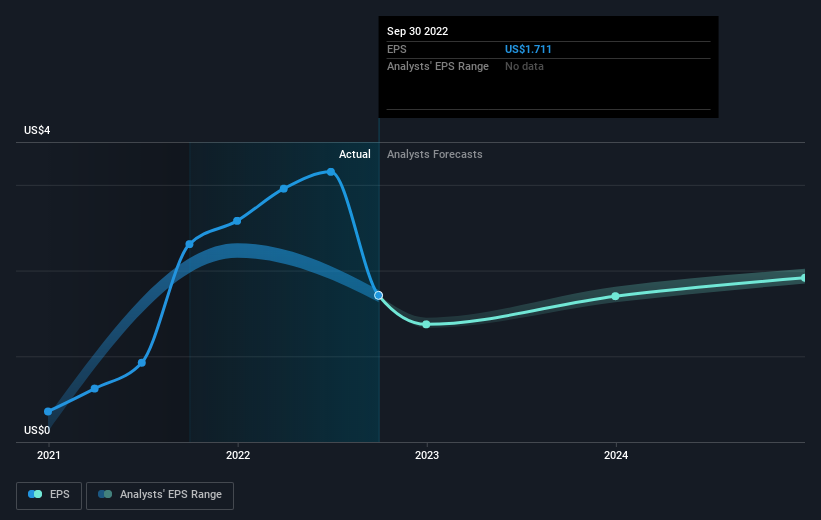

Mattel became profitable within the last three years. That would generally be considered a positive, so we’d expect the share price to be up.

The graphic below depicts how EPS has changed over time (unveil the exact values by clicking on the image).

It is of course excellent to see how Mattel has grown profits over the years, but the future is more important for shareholders. You can see how its balance sheet has strengthened (or weakened) over time in this free interactive graphic.

A Different Perspective

Mattel shareholders are down 18% over twelve months, which isn’t far from the market return of -19%. The silver lining is that longer term investors would have made a total return of 4% per year over half a decade. If the stock price has been impacted by changing sentiment, rather than deteriorating business conditions, it could spell opportunity. It’s always interesting to track share price performance over the longer term. But to understand Mattel better, we need to consider many other factors. Consider for instance, the ever-present spectre of investment risk. We’ve identified 2 warning signs with Mattel (at least 1 which is significant) , and understanding them should be part of your investment process.

Of course Mattel may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Valuation is complex, but we’re helping make it simple.

Find out whether Mattel is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

[ad_2]

Source link