[ad_1]

In order to justify the effort of selecting individual stocks, it’s worth striving to beat the returns from a market index fund. But its virtually certain that sometimes you will buy stocks that fall short of the market average returns. We regret to report that long term Leggett & Platt, Incorporated (NYSE:LEG) shareholders have had that experience, with the share price dropping 25% in three years, versus a market return of about 26%. Contrary to the longer term story, the last month has been good for stockholders, with a share price gain of 9.9%. But this could be related to good market conditions, with stocks up around 5.9% during the period.

So let’s have a look and see if the longer term performance of the company has been in line with the underlying business’ progress.

View our latest analysis for Leggett & Platt

While markets are a powerful pricing mechanism, share prices reflect investor sentiment, not just underlying business performance. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

During the unfortunate three years of share price decline, Leggett & Platt actually saw its earnings per share (EPS) improve by 7.0% per year. This is quite a puzzle, and suggests there might be something temporarily buoying the share price. Alternatively, growth expectations may have been unreasonable in the past.

Since the change in EPS doesn’t seem to correlate with the change in share price, it’s worth taking a look at other metrics.

Given the healthiness of the dividend payments, we doubt that they’ve concerned the market. It’s good to see that Leggett & Platt has increased its revenue over the last three years. If the company can keep growing revenue, there may be an opportunity for investors. You might have to dig deeper to understand the recent share price weakness.

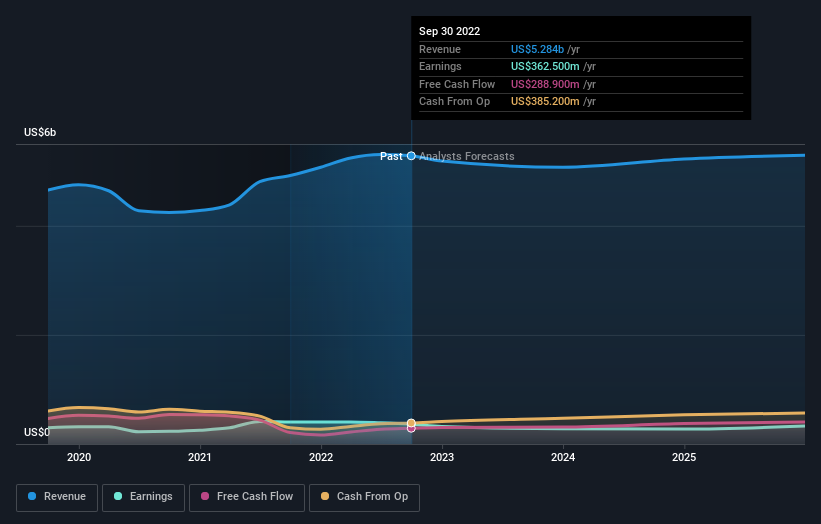

The company’s revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

Balance sheet strength is crucial. It might be well worthwhile taking a look at our free report on how its financial position has changed over time.

What About Dividends?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. It’s fair to say that the TSR gives a more complete picture for stocks that pay a dividend. In the case of Leggett & Platt, it has a TSR of -15% for the last 3 years. That exceeds its share price return that we previously mentioned. This is largely a result of its dividend payments!

A Different Perspective

Although it hurts that Leggett & Platt returned a loss of 7.3% in the last twelve months, the broader market was actually worse, returning a loss of 12%. Unfortunately, last year’s performance may indicate unresolved challenges, given that it’s worse than the annualised loss of 1.0% over the last half decade. While some investors do well specializing in buying companies that are struggling (but nonetheless undervalued), don’t forget that Buffett said that ‘turnarounds seldom turn’. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For instance, we’ve identified 2 warning signs for Leggett & Platt that you should be aware of.

But note: Leggett & Platt may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

What are the risks and opportunities for Leggett & Platt?

Leggett & Platt, Incorporated designs, manufactures, and markets engineered components and products worldwide.

View Full Analysis

Rewards

-

Trading at 2.7% below our estimate of its fair value

Risks

-

Earnings are forecast to decline by an average of 0.01% per year for the next 3 years

-

Debt is not well covered by operating cash flow

View all Risks and Rewards

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

[ad_2]

Source link