[ad_1]

A little over two weeks after a winter storm triggered thousands of flight delays and cancellations, domestic airlines were once again forced to pause operations temporarily on Wednesday. A Federal Aviation Administration (FAA) review has linked the outage, which grounded every carrier in the U.S. for the first time since 9/11, to IT personnel “who failed to follow procedures.”

Investors don’t appear to have been fazed. Shares of U.S. domestic airlines finished Wednesday up more than 1% before advancing a further 4% on Thursday in response to positive earnings estimates. Airline and travel names were the best performers in the S&P 500 on Thursday, with American Airlines jumping 9.7%, United Airlines 7.5% and Expedia Group 3.8%.

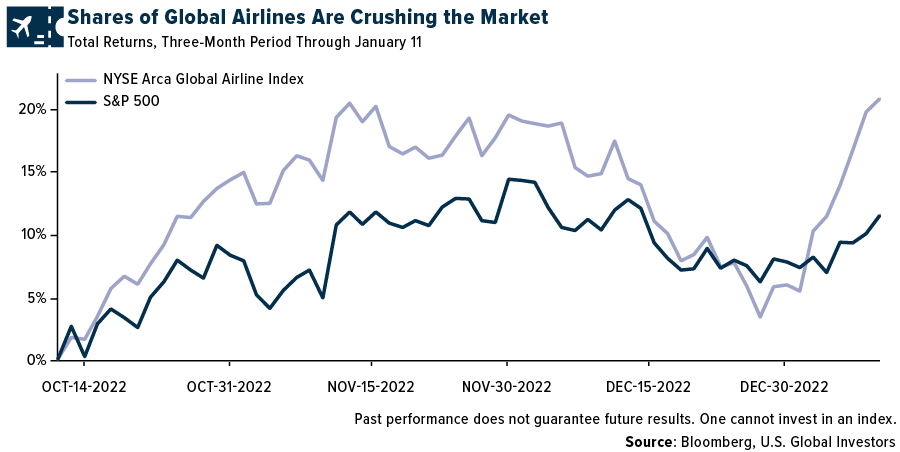

For the one-month, three-month and six-month periods, a basket of global airline stocks has crushed the market. Since the middle of October, the NYSE Arca Global Airline Index has soared over 22% compared to the S&P 500, which has gained 11%.

Much of the recent increase has been driven by China’s decision to lift quarantining requirements for incoming travelers for the first time since the start of the pandemic. Airline bookings in China have exploded as a result.

But regional air travel demand was expanding even before China’s announcement. This week, the Association of Asia Pacific Airlines (AAPA) reported that 13.4 million international passengers were carried by Asian airlines in November 2022, a phenomenal 663% increase from the same month a year earlier. Based on revenue passenger kilometers (RPKs), demand rose nearly 500% in the 12-month period through the end of November.

There are other drivers to the stock rally, though.

Optimism for Airline Earnings

It’s earnings season, and so far, only Delta Air Lines has reported fourth-quarter and full-year profits. Although profits were dented somewhat from higher expenses and debt-servicing, the Atlanta-based carrier made great progress toward reaching and surpassing 2019 levels. In the fourth quarter, net income was $828 million, still 25% away from the $1.1 billion that was generated three years earlier. However, operating cash flow came in at $1.2 billion for the quarter, $220 million more than was reported for the period in 2019.

It was American’s statement this week that really excited investors. The carrier said that its fourth-quarter profit will be double analyst expectations, and revenue will also beat, thanks to a strong holiday travel season. Preliminary filings show that revenues were as much as 17% over those generated during the year-ago period, against expectation of a 12% increase.

American is scheduled to report on January 18. Shares of the carrier have jumped almost 20% in the past week.

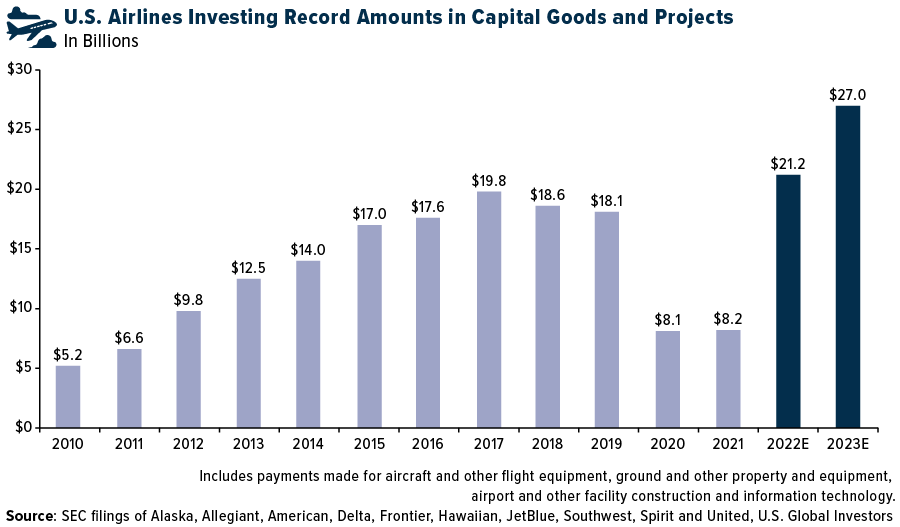

U.S. Airlines Investing Record Amounts

As an investor, I like to see when a company invests in itself, whether that means building a new facility or putting in new orders. It tells me executives are optimistic about the future and are positioning for growth.

We’re seeing airlines do just that right now. According to Airlines for America (A4A), U.S. carriers are investing a record amount on things such as aircraft, equipment, airport construction, information technology and more. In 2022, capital expenditures were estimated at $21.2 billion; this year, they’re forecast to hit $27.0 billion, which would be a record.

Both Airbus and Boeing reported strong delivery and new orders numbers for 2022. Since the tragic events involving Boeing’s 737 MAX in 2019, the Arlington-based company has been playing catchup to its main rival, and for the fourth straight year, Airbus topped its U.S. competitor. Airbus delivered 661 jets and won a net 820 new orders last year, against Boeing’s 480 jets delivered and 774 net new orders.

United Airlines was responsible for putting in one of the largest orders I’ve ever seen. In the “largest widebody order by a U.S. carrier in commercial aviation history,” the company announced in December that it ordered 100 Boeing 787 Dreamliners with an option to purchase 100 more. What’s more, United says it continues to its “unprecedented effort to upgrade the interiors of its existing fleet.”

Will Business Travel Recover in 2023? Morgan Stanley Believes So

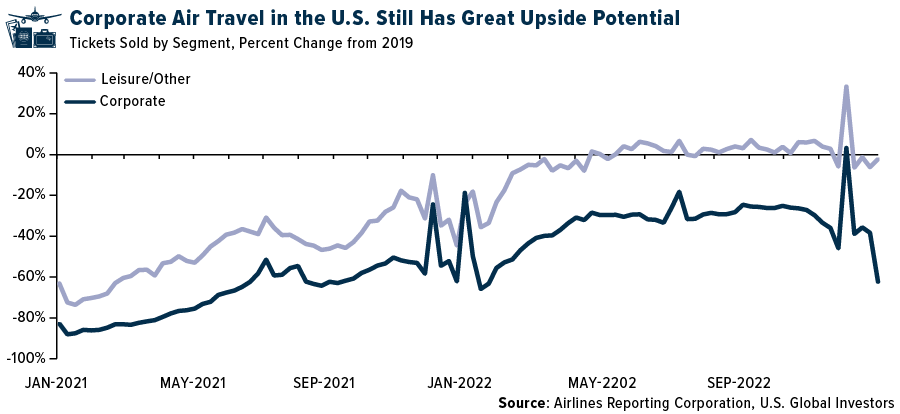

What a lot of investors are waiting for, I believe, is a sign that business travel has fully bounced back. According to data from ticket transactions settlement firm Airlines Reporting Corporation (ARC), leisure travel has safely returned to 2019 levels, whereas business travel continues to trail. Of course, that just means there’s great upside potential.

A recent report from Morgan Stanley suggests businesses are ready to start spending on corporate travel again. Based on a survey of 100 global corporate travel managers, travel budgets are expected to be 98% of 2019 levels on average. Smaller companies are leading demand, Morgan Stanley says, with nearly two-thirds of them saying they believe travel budgets will increase this year compared to 2022.

Wheels up!

In case you missed it…

This week we updated our ever-popular Periodic Table of Commodities Returns for 2022! It’s interactive, and a pdf is available for download. Explore it now by clicking here.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.00%. The S&P 500 Stock Index rose 2.67%, while the Nasdaq Composite climbed 4.82%. The Russell 2000 small capitalization index gained 5.26% this week.

- The Hang Seng Composite gained 3.57% this week; while Taiwan was up 3.14% and the KOSPI rose 4.20%.

- The 10-year Treasury bond yield fell 5 basis points to 3.502%.

Airlines and Shipping

Strengths

- The best performing airline stock for the week was United Airlines, up 21.9%. Boeing reported fourth quarter 2022 commercial deliveries of 152 aircraft, up from 99 in the same quarter the year prior, and up sequentially from 112 in the third quarter of 2022. The delivery numbers were a positive with the company only one aircraft shy of meeting its goal of 375 MAX deliveries for the full year. The consensus view was that Boeing was not going to hit its target of 375, so investors are likely to look favorably toward this result.

- UPS has implemented surcharges that will take effect on January 15, replacing the original peak season surcharges set to expire January 14. The new surcharges will be at a much lower cost than the original surcharges but be implemented similarly and in place “until further notice.”

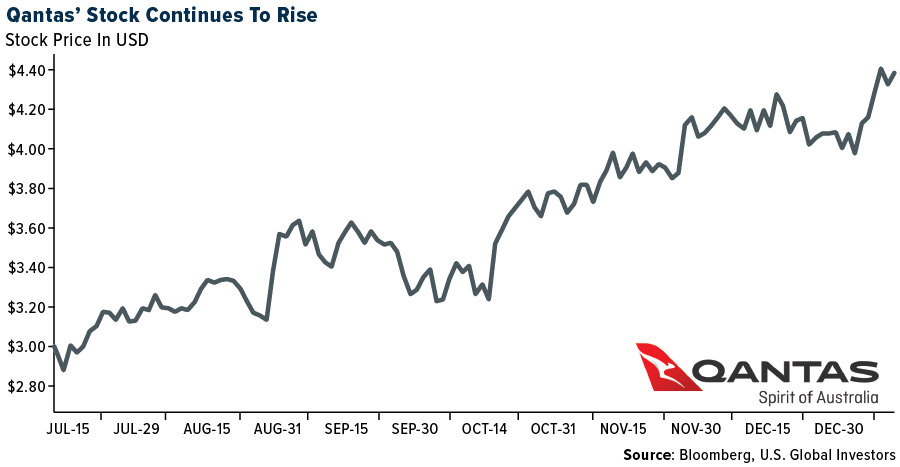

- Qantas has reason to celebrate after being named the world’s safest airline for 2023. The Australian airline has regained AirlineRatings.com’s top spot for safety, beating last year’s winner Air New Zealand by “the finest of margins.” The website considers serious incidents, recent fatal accidents, audits from aviation’s governing and industry bodies, profitability, safety initiatives, expert pilot training assessment and fleet age.

Weaknesses

- The worst performing airline stock for the week was Air Berlin, down 13.3%. For Southwest Airlines, the pre-tax impact estimate of $725-825 million for operational issues during the holidays is greater than the $600MM consensus on a slightly higher cancellation figure of 16,700. This was toward the upper end of investor expectations. It implies $43-50,000 per cancelled flight, which is greater than consensus of $35-45,000.

- The ClarkSea Index has fallen in recent weeks to $25,232 per day (from around $44,000 in May 2022). This fall likely reflects a combination of weakening macro factors, seasonality, and lower container rates. LNG prices have been falling sharply with the forward curve for both 2023 and 2024 down to $22-$23/MMBtu compared to prices above $30/MMBtu just a few weeks ago.

- Airbus reported that it delivered 661 aircraft in 2022, below consensus of 680. Airbus has not published any update on its financial results. Consensus is reducing its forecast for 2023-2025E aircraft deliveries by 3-4% per year and reducing its 2023-2025E earnings per share by 5-6% per year.

Opportunities

- The BMO Air Travel Demand Survey, conducted in late December to a sample of representatives of the Canadian population, revealed a continued robust outlook for air travel demand. A majority of respondents dismissed Covid as a deterrent to travel. Travelers intend to take the same or more frequent trips and spend the same or more on travel in 2023, particularly in the leisure segment. Travelers’ interest in destinations is broad, with opportunities to upgrade the travel experience through cabin upgrades or purchase of extra legroom, which was voted as the most valued option/add-on by travelers.

- Morgan Stanley’s Shipper Survey shows an uptick in the overall macro-outlook and stabilizing inventory levels with a continued unprecedented rate of destocking, which means elevated inventory risk is likely past. The group has previously established that the inventory data in its Shipper Survey closely tracks the pricing through cycles. Surveys have also seen improvement in current supply and rate sentiment relative to underperformance all year.

- Out of the big four airlines, United is showing the most aggressive first quarter 2023 domestic capacity, up 4.7% versus 2019 followed by Delta Air Lines (up 1.6%), Southwest (down 1.1%) and American Airlines (down 1.8%). American had the most material first quarter domestic capacity cuts this month as current schedules are -0.7% points lower than last month’s schedules.

Threats

- According to JPMorgan, the Southwest IT picture remains unclear. The bank has been assuming $800 million or so of 2023 IT spend, and – prior to the meltdown – it would have identified overall IT as an area of relative weakness for Southwest. Granted, they have no expertise in crew scheduling software, but if an airline can’t feasibly operate red-eyes or tell you if your bag has been loaded, the base assumption is that systems aren’t state of the art.

- Labor unrest took an unusually heavy toll on ports around the world last year, and the outlook for continued economic instability could bring even more upheaval to global supply chains in 2023. There were at least 38 instances of protests or strikes affecting port operations last year, more than four times as many as in 2021 when the pandemic upended global trade, according to Crisis24, a maritime security consultancy.

- March quarter capacity has been reduced by Hawaiian Airlines and Alaska Airlines. The Hawaiian reduction was entirely related to international routes while the Alaska reduction was greatest in the Seattle and Portland hubs. Alaska also reduced its June quarter schedule by 1.3% over the same period. It is likely that early summer schedules will need to be revised down over the next several weeks before reflecting actual capacity expectations.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Poland, gaining 2.9%. The best performing country in Asia this week was the Philippines, gaining 4.3%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 4.9%. The Indonesia rupiah was the best performing currency in Asia this week, gaining 3.3%.

- The United States reported a drop in inflation this week, prompting the dollar to weaken and pushing emerging markets currencies higher. This week we have seen inflation pressure easing in the Czech Republic, Poland, Romania, and Greece. China’s consumer price index (CPI) increased to 1.8% in December from 1.6% in November.

Weaknesses

- The worst performing country in emerging Europe for the week was Turkey, losing 6.7%. The worst performing country in Asia this week was Indonesia, losing 0.5%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 0.4%. The Philippine peso was the worst relative performing currency in Asia this week, gaining 0.8%.

- The Istanbul Stock Exchange has corrected, year-to-date, and has become the world’s worst performing market so far in 2023. Rising political tensions caused panic selling among local investors, triggering market-wide circuit breakers for a second time this year.

Opportunities

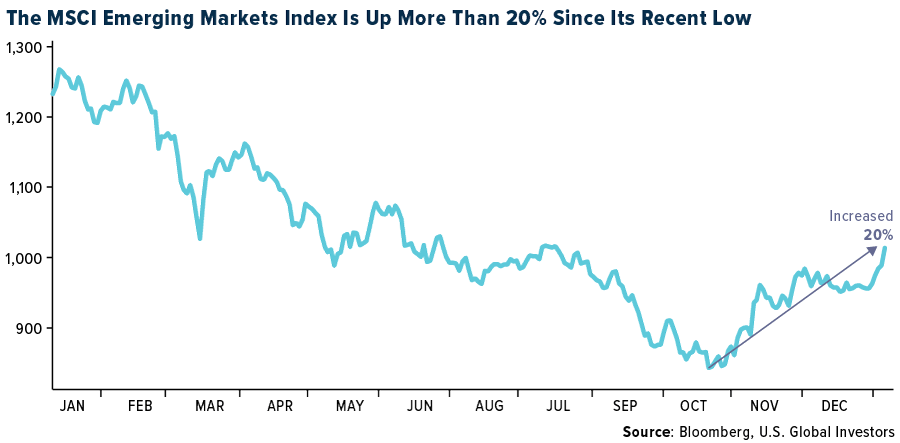

- The MSCI Emerging Markets Index recorded strong returns at the beginning of the year in 2023, appreciating more than 20% since its most recent low that took place back in October of 2022. Technically, a bull market starts when stocks gain more than 20% from recent lows.

- Taiwan Semiconductor, the world’s largest semiconductor producer, reported stronger sales in the fourth quarter, but the company announced spending cuts in 2023 as it expects sales weakness ahead. However, the company indicated that the second quarter could be the revenue bottom for the year. The Taiwan and South Korea markets have higher exposure to semiconductor names.

- The World Health Organization warned that the Lunar New Year holiday in China, which officially starts on January 22, may lead to increased Covid infections. However, Chinese media reported many parts of China are already past their peak in Covid infections with cases declining in Beijing and several major provinces. For example, 90% of Henan’s 100 million residents had been infected with Covid already.

Threats

- The Chinese government suspended issuing short-term visas for South Korea and Japan in Beijing’s first retaliatory move against Covid curbs on travelers from China. Due to the recent spike in Covid cases in the mainland, many countries require passengers from China to have a negative pre and post departure Covid PCR test.

- Bloomberg cited independent demographer He Yafu, ahead of official statistics next week, who said China’s birth rate will likely have fallen to a new low of around 10 million in 2022. If confirmed, it would be the seventh consecutive year of birth rate declines and the lowest since 1949. Deaths were likely to top 2021’s 10.1 million, in part because of Covid, meaning China’s overall population may have declined overall in 2022.

- Major provinces in China and large cities may have passed peak Covid infections, but the Covid wave may move to rural areas next (which are not as densely populated but where medical resources are relatively scarce). Reuters cited Zeng Guang, former chief epidemiologist at the China CDC, who said China’s Covid wave peak is expected to last another two to three months and will soon hit the country’s countryside.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was lumber, up 17.12%, after slumping to its lowest price in more than two years last week. Expectations for further strength are considered low. EU storage is on pace to exit the winter 50% full, two times the level last year, and reducing the 2023 call on LNG while freeing up cargos for rising China demand. While the global LNG market is still tight, 2023-2024 prices no longer need to reflect a large risk premium for potential storage and supply shortfalls.

- According to Cantor, with U.S. conversion capacity set to come back on-line mid-year, this could create the dynamic of normalizing uranium prices (which more than doubled last year) with the more substantial price gains finally cascading down the nuclear fuel cycle to mined uranium oxide.

Against this positive backdrop, Cantor notes the Sprott Physical Uranium Trust has regained its NAVPU premium. Spot market volumes remain exceedingly thin, and the group expects the uranium oxide price action will likely be meaningfully higher and fast. - Base metals surged on optimism over China’s economic recovery, bets for a more dovish Federal Reserve, and low exchange stockpiles. China should return to “normal” growth soon as Beijing steps up support for households and businesses, Guo Shuqing, party secretary of the country’s central bank, told state media. That’s adding to hopes that the government will expand measures to steady the economy in the wake of a massive wave of Covid-19 infections.

Weaknesses

- The worst performing commodity for the week was natural gas, down 6.36%, on demand weakness, ample storage, and mild weather. Chinese lithium prices dropped 1-3% this week on lower spot demand. Traders continue to cut prices further with some producers also lowering prices.

- Chinese iron ore futures fell 3% as the government looks to target illegal trading once again, Bloomberg reports. Specifically, the NDRC cites that: 1) it is “highly concerned” about recent iron ore price changes; 2) there are obvious speculative elements in the recent price rally as market fundamentals remain stable; and 3) it will crack down further on illegal activities, hereunder showing zero tolerance for “spreading false information, driving up prices and malicious speculation.”

- U.S. coal prices plunged from record highs as warm winter conditions eased demand for the dirtiest fossil fuel, writes Bloomberg. Coal from the Northern Appalachia region slumped to $115 a ton for the week, down 45% from the prior week, according to government figures released Monday.

Opportunities

- Goldman remains constructive on the European oil sector at this complex macro juncture for three reasons: 1) strong balance sheets: European oils have taken advantage of strong cash generation to strengthen their balance sheet, with net debt/equity at 6% by end 2023E compared to a long-term range of 15-30%; 2) resilient free cash flow (FCF) and ongoing capital discipline, with the sector still generating a 17% FCF yield in 2023E, at the current forward curve; 3) underinvestment and supply tightness, which they discuss in detail in their Top Projects 2022 report, suggesting a structural production decline in most non-OPEC and several OPEC countries.

- The market expects solid global oil demand growth of 2.7mb/d in 2023 to push the market back into deficit in the second half of the year and raise Brent to $105 per barrel by the fourth quarter of 2023. This tightening should then allow OPEC to unwind its October production cut in the second half. However, if the market turned out to be softer, then OPEC could stick to its October cuts or cut production even further given its significant pricing power. Overall, this “OPEC put” limits the downside risks to the bullish oil price forecast.

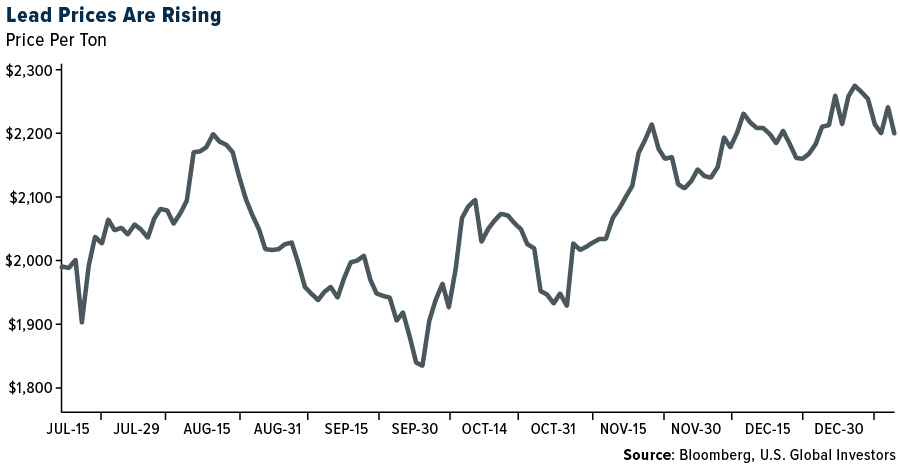

- Lead isn’t a glamorous commodity, but it’s been delivering handsome returns as of late, and that makes it a raw material to watch closely. Benchmark prices soared by 20% in the final quarter of last year as demand outpaced supply and widely-tracked stockpiles were depleted. If those drivers are sustained, further gains are possible, reports Bloomberg.

Threats

- New research on internal climate projections at Exxon Mobil shows its scientists correctly predicted that the burning of fossil fuels would lead to a rise in global temperatures by roughly 0.20 degrees every decade. The study covered materials from 1977 through 2003, according to Bloomberg. Patrick Parenteau, a professor of law emeritus at Vermont Law and Graduate School, noted “This analysis is a stock of dynamite,” to those states that have opened investigations against Exxon on misleading investors and the public on what the company knew concerning the burning of fossil fuels.

- The billionaire at the center of last year’s nickel short squeeze is planning a major shift in his production mix, reports Bloomberg, in a move that could reshape global supply dynamics and inject fresh volatility into the battered nickel market. Xiang Guangda’s Tsingshan Holding Group Co. is seeking to profit from an unusually large premium in the price of refined nickel metal – the type that is deliverable on exchanges in London and Shanghai – over the intermediate forms that Tsingshan supplies for battery manufacturing, according to people familiar with the matter.

- Energy equities were the top-performing group in 2022, outperforming the wider market (MSCI World) by 50%. Given the drop in crude pricing, this puts the sector at risk, should recession fears worsen and as there is some tactical profit taking from the prior year’s best performers. This risk may be short lived, with factors such as cooling inflation and a potential Fed pivot, China reopening adding tailwinds to oil demand, and firming prices through the year.

Luxury Goods

Strengths

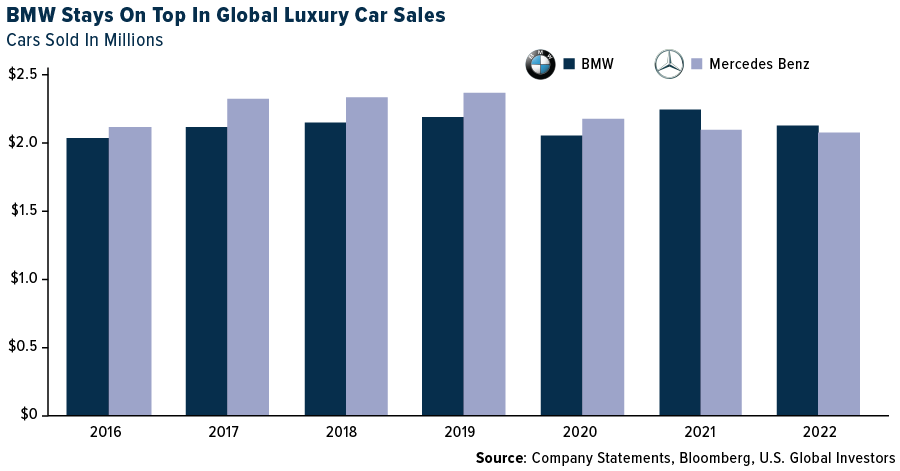

- Worldwide BMW car sales fell 5% to 2.1 million last year, but the company was able to outpace Mercedes Benz’s sales for the second year in a row. Both brands grew sales in the final months of 2022, but unfortunately could not compensate for the business lost during the first half.

- Bloomberg reported that Tesla has overtaken BMW to become the top luxury car brand in the United States for 2022, becoming the first American vehicle in 25 years to hold that title. In the United States, Tesla sold over 491,000 cars in 2022 compared to BMW, that sold close to 332,400 cars during the period, according to estimates by the Automotive News Research & Data Center.

- Faraday Future Intelligence, an electric vehicle company, was the best performing S&P Global Luxury stock for the week, gaining 57.21%. Shares gained last week after losing 94.54% in 2022. Bloomberg reported that the company received a de-listing risk warning from Nasdaq for its failure to hold an annual meeting in 2021. The company has yet to hold a meeting of shareholders within 12 months of the fiscal year ending December 31, 2021, according to an SEC filing on Tuesday.

Weaknesses

- In the last half of 2022 the sales of homes priced at $10 million and more fell sharply in some of the wealthiest parts of the country, according to a new report from the brokerage firm Serhant. Signed contracts for condos and co-ops priced at $10 million or more in New York City plummeted 68% in the second half of 2022. In Miami, the signed contracts fell 60% during the same period, Bloomberg reported.

- Tesla is cutting car prices in an attempt to increase sales. Price cuts in the U.S., announced late Thursday, were on its global top-sellers the Model 3 sedan and Model Y crossover SUV (between 6% and 20%), Reuters calculations showed. The basic version of its Model Y now costs $52,990, down from $65,990 previously.

- Luk Fook Holdings, a Chinese jewelry and watch retailer, was the worst performing S&P Global Luxury stock for the week, losing 6.5%. Shares declined after the company announced weaker store sales.

Opportunities

- Inflation in United States eased to 6.5% in December from 7.1% in November. The dollar slipped and risky assets gained on the news. Lower inflation leaves more room for consumers to spend extra on luxury goods and services.

- The secondary market for luxury watches is expected to surpass the primary market by 2033. The market for vintage and pre-owned watches will surge to 79 billion euros ($85 billion) in 2033, more than triple the 25 billion euros sold last year, Luxe Consult, a Swiss-based industry analyst and consultant firm, forecast. Some sellers and dealers charge a premium above retail prices for the most in-demand watch models.

- The Spring Festival in China starts on January 22 this year but travel due to the Lunar New Year holiday has already begun. Many high-end brands have been preparing for China to remove travel restrictions and ease Covid measures. Now, 2 billion passenger trips are expected during the broader Luna New Year travel period, which starts January 7 and will run for 40 days, FactSet reported.

Threats

- Luxury stocks recorded solid gains, year-to-date, following already strong performance in the last quarter of 2022. In the short term, technical charts suggest that a correction may follow. However, in the long term, luxury stocks could continue to climb higher after reaching a bottom in October of 2022.

- The travel recovery between China and Hong Kong will be gradual. Blomberg reported that mainland China visitations to Hong Kong in 2023 could reach 63% of pre-Covid levels. Currently, there is a limit of 60,000 daily entries allowed and depending on the Covid situation, the current limit of 60,000 visitors could be relaxed or restricted further.

- Bloomberg economists are predicting that retail sales will weaken in the United States. Economic data will be announced on Wednesday, January 18.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Gala, rising 127.81%.

- A prolonged rally in Bitcoin is giving crypto enthusiasts a smidgen of something to be happy about during a dark period for the industry. The world’s largest token has advanced for nine straight days, reports Bloomberg, the longest such streak since 2020.

- Nike won a round in its trademark infringement lawsuit against sneaker marketplace StockX LLC, when a Manhattan federal judge declined to force the athletic-wear company to disclose the money it makes from shoes, digital sneakers and NFTs, according to Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Fei USD, down 2.42%.

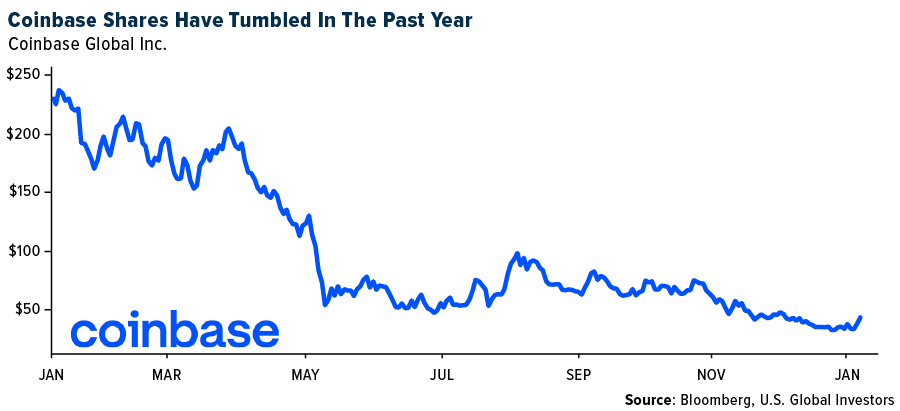

- Coinbase Global is firing about 950 employees, or about 20% of its workforce, as the worsening crypto slump spurs another round of layoffs at the biggest U.S. digital-asset exchange. Co-founder and CEO Brian Armstrong announced the job reductions in a blog post Tuesday, reports Bloomberg, saying the steps were needed to weather the industry downturn. In June of last year Coinbase announced it would lay off 18% of its workforce, the equivalent of roughly 1,200 employees. It eliminated another 60 positions in November and will now shut down several projects.

- Ferrari’s Formula One Team has ended its partnership with blockchain technology company Velas Network, as deals between sports companies and firms in the beleaguered cryptocurrency sector continues to crumble. Crypto companies were becoming big spenders in sports sponsorships, aggressively courting retail investors globally through a flood of big-ticket deals, writes Bloomberg.

Opportunities

- A new collection called Win Trump Prizes, that allows users to buy rewards related to former U.S. president Donald Trump, has launched on OpenSea. Individuals can claim a one-on-one Zoom meeting with Trump for 200 ETH, a gala dinner ticket for 50 ETH, a meeting with Trump for 21.45 ETH, and more. The collection has a trading volume of 35 ETH with 669 owners, according to an article published by Bloomberg.

- Crypto market maker CyberX has raised $15 million in a strategic investment from Foresight Ventures, a crypto venture capital firm with about $400 million in assets under management. CyberX will use the funds to expand its teams in Asia and North America, add more integrations with exchanges and decentralized finance protocols, and build out its trading infrastructure, writes Bloomberg.

- Bitcoin has defied bad tidings to register its best week since 2021. The largest digital currency gained roughly 12% so far this week and is on pace for its best weekly performance since October 2021, writes Bloomberg.

Threats

- Former FTX engineering chief Nishad Singh met with federal prosecutors in a bid to become the third member of Sam Bankman-Fried’s inner circle to seek a cooperation deal in the fraud case over the cryptocurrency exchange’s collapse, reports Bloomberg.

- Crypto lender Nexo’s office in Sofia was raided by Bulgarian police on Thursday as part of an investigation into suspected money laundering and tax crimes. More than 300 police officers, prosecutors and national security agents are taking part in the operation. In total, police searched 15 addresses related to Nexo, writes Bloomberg.

- Sam Bankman-Fried offered one of his most detailed descriptions yet of the FTX debacle as he prepares to fight fraud charges, blaming crashing markets and an attack from a rival for the eventual bankruptcy of his exchange. “I didn’t steal funds, and I certainly didn’t stash billions away,” the former crypto magnate wrote in a blog post Thursday, reports Bloomberg.

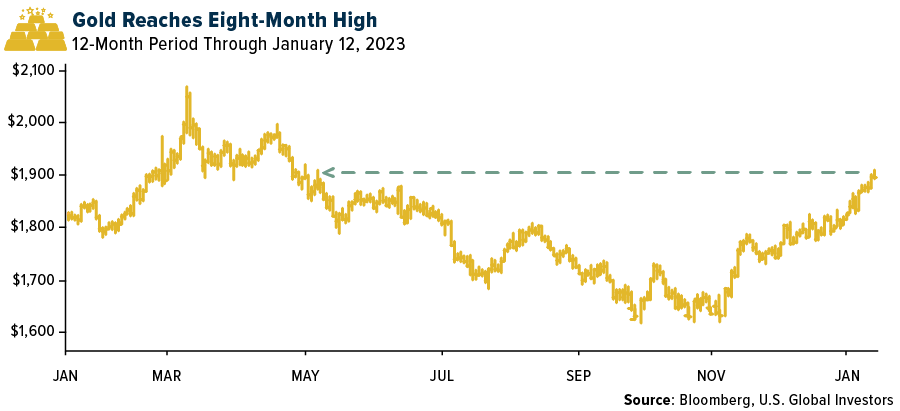

Gold Market

This week gold futures closed at $1,924.20, up $54.50 per ounce, or 2.91%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.92%. The S&P/TSX Venture Index came in up 5.71%. The U.S. Trade-Weighted Dollar fell 1.65%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-12 | CPI YoY | 6.5% | 6.5% | 7.1% |

| Jan-12 | Initial Jobless Claims | 215k | 205k | 206k |

| Jan-16 | China Retail Sales | -9.5% | — | -5.9% |

| Jan-17 | Germany CPI YoY | 8.6% | — | 8.6% |

| Jan-17 | Germany ZEW Survey Expectations | -15.0 | — | -23.3 |

| Jan-17 | Germany ZEW Survey Current Situation | -57.0 | — | 61.4 |

| Jan-18 | Eurozone CPI Core YoY | 5.2% | — | 5.2% |

| Jan-18 | PPI Final Demand YoY | 6.8% | — | 7.4% |

| Jan-19 | Housing Starts | 1,358k | — | 1,427k |

| Jan-19 | Initial Jobless Claims | 212k | — | 205k |

Strengths

- The best performing precious metal for the week was gold, up 2.91%. Lundin Gold reported another strong quarter with fourth-quarter production of 121,000 ounces, ahead of consensus and bringing full-year output to 476,000 ounces, above the high end of guidance of 470,000 ounce. “I am extremely happy to announce that for the second year running, Lundin Gold has beaten its production guidance,” Ron Hochstein, President and CEO, commented. “We continue to push the boundaries of what Fruta del Norte is capable of, and noteworthy improvements have been made across the board as compared to last year.”

- Gold headed for a fourth weekly gain, reports Bloomberg, following data that showed U.S. inflation is cooling, buoying expectations that the Federal Reserve will rein in aggressive interest-rate hikes. Bullion notched an eight-month high on Friday, the article continues, extending a rally that started in early November on signs the Fed was becoming less hawkish.

- A survey of 13 local Russian banks last year states that Russian citizens bought 57 tonnes of gold in 2022, as they sought to safeguard their savings following the invasion of Ukraine (and also took advantage of the cancellation of the local tax on bullion buying), cites Vedomosti newspaper. The purchases represent 1.8 million troy ounces, which accounts for more than 15% of domestic output. In 2021, there were only 193,000 ounces purchased through these banks.

Weaknesses

- The worst performing precious metal for the week was platinum, down 2.65%, on little market news following three consecutive weeks of gains. Triple Flag Precious Metals reported fourth quarter GEO sales of 25,400 ounces and revenue of $43.9 million, versus consensus of 27,500 ounces and $47.8 million, respectively. For the full year 2022, GEO sales were 84,600 ounces and revenue was $151.9 million, versus consensus of 87,000 ounces and $156 million, respectively (based on actual 2022 commodity prices). The company was guiding sales toward the lower end of the 2022 guidance range of 88–92,000 GEOs.

- New Gold produced 81,000 ounces of gold and 6.9 million pounds of copper (20% below consensus). Production results were driven by higher head grades; mill throughput rates at both assets were well below consensus. That said, the company achieved the mid-point of full-year (revised) guidance.

- Victoria Gold said it produced 43,741 ounces of gold

during the fourth quarter, which ended on December 31, 2022, compared with 50,028 ounces in the third quarter. Full-year 2022 production from the Eagle Gold Mine, part of the company’s 100%-owned Dublin Gulch gold property in central Yukon Territory, was 150,182 ounces. This was down from 164,222 ounces in 2021, Victoria Gold said.

Opportunities

- Royal Gold announced that it has acquired two portions of a gross smelter royalty that together cover a large area including the Cortez mine operational area and the entirety of the Fourmile development project in Nevada for $204.1 million in cash. The royalties acquired are a 0.24% gross royalty covering areas including the Pipeline and Crossroads deposits and a 0.45% gross royalty covering areas including the Cortez Hills, Goldrush, Fourmile and Robertson deposits.

- Gold may be a decent candidate for a return to bull market territory in the first half of 2023 as the positives mount. Concerns about a global slowdown, a weaker dollar, and lower real rates are burnishing bullion’s allure, as are further signs of significant buying by central banks.

- “Dr Doom” Nouriel Roubini was recently interviewed by Business Insider, and he predicts the Federal Reserve will not have the stomach to raise rates past 6% to bring inflation down to target levels due to potential recession risks. Roubini noted that gold is the best bet for investors as inflation, high debt, and extreme volatility are in store for the future economic cycle.

Threat

- Jeff Currie believes the best China reopening trade is oil. He says crude oil is heading higher to $110 by the third quarter of 2023. This could send a secondary inflation wave through the mining sector unless management considers locking in some fuel hedges while prices are relatively low. In addition, exports of Russian diesel to Europe are set to end in three weeks. Europe was getting about 50% of its diesel from Russia but lowered that to 40% by December. The diesel squeeze could potentially impact prices globally. It is likely some Russian diesel will be resold by India or China back into international markets.

- “If the market were to switch to the Fed’s path, the gold price would risk suffering a considerable setback,” Commerzbank AG analysts including Carsten Fritsch wrote in a note. Gold exchange-traded fund investors “also appear to take this view, as they are still exercising restraint with purchases despite the steep price rise,” the bank wrote.

- North America’s top mining CEOs are anticipating turbulent times ahead, reports Bloomberg. Mark Bristow, CEO of Barrick Gold, noted that he is not sure if anywhere is perfectly safe to invest in right now. This will be seen as the start of serious change – particularly in the way mines operate and are held accountable. Recently, First Quantum Minerals and Panama’s government have been in dispute on the future minimum taxation plan the government is demanding.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/30/22):

Lundin Gold

New Gold

Victoria Gold

Royal Gold

K92 Mining

Dundee Precious Metals

Boeing Co/The

United Parcel Service

Qantas Airways

Airbus SE

United Airlines

Delta Air Lines

American Airlines

Southwest Airlines

Hawaiian Holdings

Alaska Air Group

Bayerische Motoren Werke

Mercedes-Benz Group

Tesla Inc.

Taiwan Semiconductor

Airbus SE

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The ClarkSea Index is a weighted average index of earnings for the main vessel types where the weighting is based on the number of vessels in each fleet sector.

The NYSE Arca Global Airlines Index is a modified equal-dollar weighted Index designed to measure the performance of highly capitalized and liquid U.S. and international passenger airline companies identified as being in the airline industry and listed on developed and emerging global market exchanges.

[ad_2]

Source link