[ad_1]

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss making companies can act like a sponge for capital – so investors should be cautious that they’re not throwing good money after bad.

If this kind of company isn’t your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Man Wah Holdings (HKG:1999). While this doesn’t necessarily speak to whether it’s undervalued, the profitability of the business is enough to warrant some appreciation – especially if its growing.

Check out our latest analysis for Man Wah Holdings

How Quickly Is Man Wah Holdings Increasing Earnings Per Share?

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. So it makes sense that experienced investors pay close attention to company EPS when undertaking investment research. It certainly is nice to see that Man Wah Holdings has managed to grow EPS by 18% per year over three years. As a general rule, we’d say that if a company can keep up that sort of growth, shareholders will be beaming.

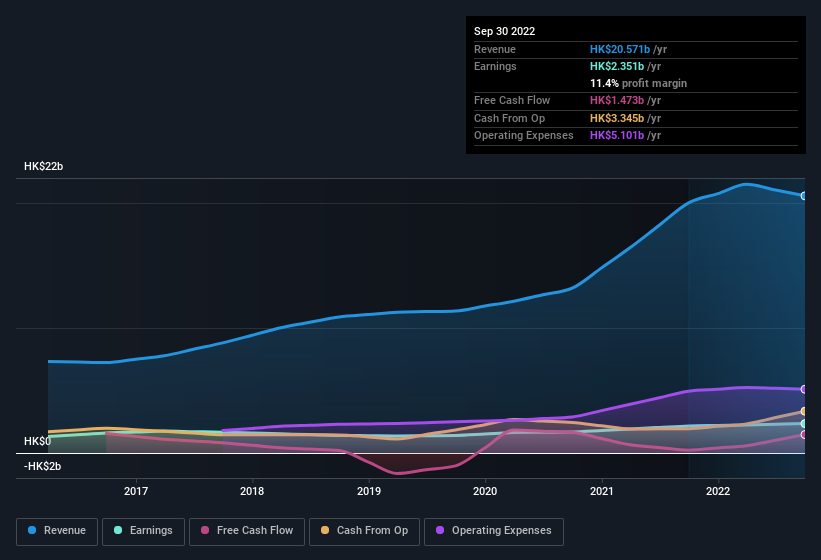

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. While we note Man Wah Holdings achieved similar EBIT margins to last year, revenue grew by a solid 2.8% to HK$21b. That’s a real positive.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

Of course the knack is to find stocks that have their best days in the future, not in the past. You could base your opinion on past performance, of course, but you may also want to check this interactive graph of professional analyst EPS forecasts for Man Wah Holdings.

Are Man Wah Holdings Insiders Aligned With All Shareholders?

It’s said that there’s no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

One gleaming positive for Man Wah Holdings, in the last year, is that a certain insider has buying shares with ample enthusiasm. Specifically, in one large transaction Chairman Man Li Wong paid HK$33m, for stock at HK$6.67 per share. Seeing such high conviction in the company is a huge positive for shareholders and should instil confidence in their mission.

And the insider buying isn’t the only sign of alignment between shareholders and the board, since Man Wah Holdings insiders own more than a third of the company. To be exact, company insiders hold 61% of the company, so their decisions have a significant impact on their investments. This should be seen as a good thing, as it means insiders have a personal interest in delivering the best outcomes for shareholders. at the current share price. That level of investment from insiders is nothing to sneeze at.

Shareholders have more to smile about than just insiders adding more shares to their already sizeable holdings. That’s because Man Wah Holdings’ CEO, Man Li Wong, is paid at a relatively modest level when compared to other CEOs for companies of this size. The median total compensation for CEOs of companies similar in size to Man Wah Holdings, with market caps between HK$16b and HK$50b, is around HK$4.6m.

The Man Wah Holdings CEO received total compensation of just HK$2.2m in the year to March 2022. That’s clearly well below average, so at a glance that arrangement seems generous to shareholders and points to a modest remuneration culture. CEO compensation is hardly the most important aspect of a company to consider, but when it’s reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of good governance, more generally.

Does Man Wah Holdings Deserve A Spot On Your Watchlist?

You can’t deny that Man Wah Holdings has grown its earnings per share at a very impressive rate. That’s attractive. On top of that, insiders own a significant piece of the pie when it comes to the company’s stock, and one has been buying more. These things considered, this is one stock worth watching. Before you take the next step you should know about the 1 warning sign for Man Wah Holdings that we have uncovered.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Man Wah Holdings, you’ll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we’re helping make it simple.

Find out whether Man Wah Holdings is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

[ad_2]

Source link